Survivor Planning

By Elaine Floyd, CFP ®

Survivor benefits are one of the most valuable—and under-appreciated—forms of Social Security. Maximizing this form of life insurance requires planning while both spouses are alive and also following the death of one spouse.

A maximum earner we’ll call David, who is age 62 now and who claims his benefit at age 70 can, upon his death at 85, provide his wife, Debbie, with an annual, COLA-adjusted income of close to $100,000. If Debbie lives another 10 years she’ll receive more than $1 million in survivor benefits. This is about $700,000 over and above the amount she would receive on her own if her benefit were about half of his. In other words, when maximized, Social Security could be equivalent to a $700,000 life insurance policy. At no cost to you.

There are two aspects to survivor planning. The first phase starts while everyone is still alive. The second phase kicks in when one spouse dies.

Survivor planning phase 1—everyone still alive

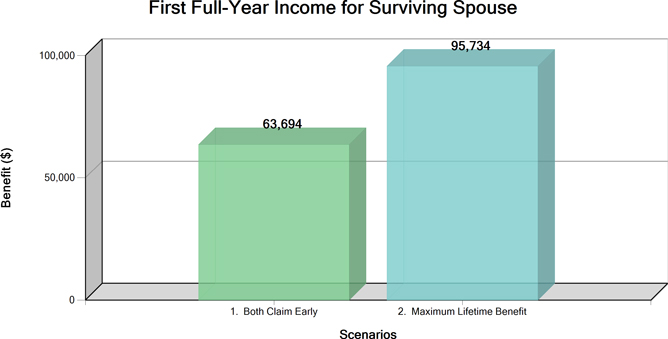

For married couples the planning centers on when the higher-earning spouse should claim, understanding that when the higher-earning spouse dies, that higher benefit will transfer over to the surviving spouse as a survivor benefit. Our Savvy Social Security Planning Software shows in graphic form the first-year survivor income under the various claiming scenarios to make it clear that if the higher earner delays to age 70, this will maximize income to the surviving spouse. Survivor planning is something many people don’t think about but it’s a very important part of the Social Security claiming analysis for married couples. Maximizing Social Security means maximizing lifetime income over the life expectancies of both spouses.

Anyone who has divorced after ten years of marriage will want to keep tabs on their ex. If you are still single or if you remarried after age 60, you may be eligible for divorced-spouse survivor benefits if your ex-spouse dies. In all likelihood your ex won’t die until you have already started your own benefit (i.e., after age 70); then it will be a matter of comparing the survivor benefit to your own benefit and switching to the survivor benefit if it is higher. But if your ex dies before then, you’ll want to coordinate your survivor benefit with your own retirement benefit. Your financial advisor can help with this.

If you are in a committed relationship and not married, Social Security may give you a reason to get married, especially if you are in your 50s or 60s. If there is an income disparity between partners, marriage will give the lower-earning partner access to survivor benefits if the higher-earning partner dies first. You must be married at least nine months to qualify for survivor benefits.

Survivor planning phase 2—following death of a spouse

Once a spouse has died, the surviving spouse may have options as to the claiming of survivor benefits and how it coordinates with their own retirement benefit.

Older widows

The most typical situation is when a couple grows old together and one spouse dies. At that point, you as the surviving spouse will call SSA and make an appointment to apply for the survivor benefit. If your own benefit is higher, you’ll keep that benefit. If not, you’ll switch to the higher survivor benefit, which will generally be equal to your spouse’s benefit at the time of death. It’s at this point that you will thank your spouse for filing at age 70 because your income will be considerably higher than if they had filed earlier.

Younger widows

If you were widowed at a young age, you become entitled to survivor benefits as early as age 60 (50 if disabled). However, if you take your survivor benefit at this early age, the benefit will be nearly 30% lower than if you were to wait until your full retirement age (67 if born in 1960 or later). You must be unmarried to collect your survivor benefit at age 60. If you are claiming later than age 60 you can be married as long as you remarried after age 60. (Let this be a warning to widows contemplating remarriage: Wait until after you turn 60 to tie the knot.)

At the time of your spouse’s death, SSA calculated a “death PIA” approximately equal to the decedent’s primary insurance amount—that is, the amount his retirement benefit would be if he had lived and worked to full retirement age. If he was a maximum earner, this could be as high as $4,000. If you were to make an appointment with SSA upon turning 60, you might be encouraged to go ahead and apply for the survivor benefit right then. But early claiming would cause the benefit to be permanently reduced, so it may not be the best move.

There’s also your own retirement benefit to think about. Ideally, you’ll want to coordinate the two benefits. The two possible strategies are to: 1) start the survivor benefit at 60 and switch to your own retirement benefit at 70, or 2) start your own retirement benefit at 62 and switch to your full survivor benefit at FRA. Which strategy you’ll choose depends on which of the two benefits is higher. Your financial advisor can help.

Earnings test applies to all benefits received before FRA. Please note that the earnings test applies to all benefits received before FRA. If you work, one dollar in benefits will be withheld for every two dollars earned over the annual threshold.

Taxation is the same. Survivor benefits are taxed the same as retirement benefits. If provisional income is over $34,000 (if single), up to 85% of benefits will be subject to federal income tax.

GPO no longer an issue. Prior to the passage of the Social Security Fairness Act in January 2025, widows who worked in jobs not covered by Social Security had their survivor benefits reduced by two-thirds of their pension amount. Now that the GPO has been repealed, even if you worked in a noncovered job you can receive your full survivor benefit (subject only to early-claiming reductions) along with your full pension.

Summary

Social Security survivor planning means first maximizing the potential survivor benefit by having the higher-earning spouse claim at 70 (and having unmarried couples marry, if appropriate), and then maximizing the actual survivor benefit by having the widow claim at the appropriate time, while also coordinating the survivor benefit with the widow’s own retirement benefit. It will be necessary for you to interact with SSA in order to obtain the amount of the survivor benefit, but you should not necessarily follow the standard advice to start the survivor benefit as early as possible. Once you know the amount of your survivor benefit you should come back to your financial advisor for planning and advice.